HLB is a world-wide accounting network of which GHJ is a member. Originally published by HLB member firm HAMT, located in Dubai, UAE, the below blog is your guide to VAT in the UAE. Find out more on how your international business will be affected and possible implementation challenges.

UAE is one of the most competitive economies in the Middle East and North Africa region. Had not been for the economic diversification policy UAE adopted, the economy of the country would have remained stagnant. As such, competing with other powerful economies would have been out of bounds.

The UAE was highly reliant on oil for centuries and in a move to reduce its dependence on oil and diversify its economy, the country implemented Value Added Tax, on January 1, 2018. Apart from UAE, Saudi Arabia is the other GCC country that introduced VAT at a standard rate of 5 percent.

Positive Steps Towards Diversification

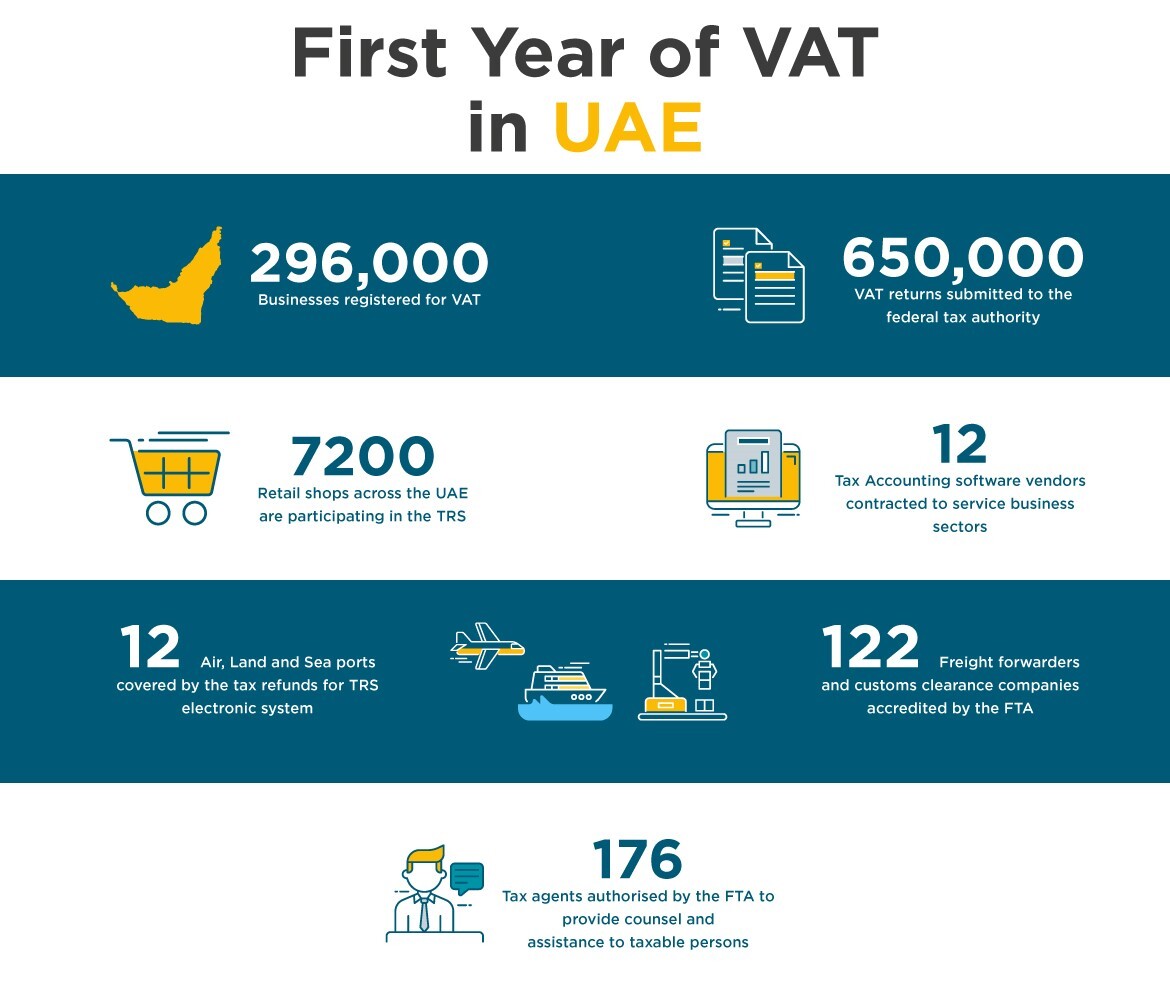

The introduction of VAT in UAE is seen as a positive step towards diversification of revenue and the initiative has been successful despite the initial few challenges. A total of 296,000 businesses registered for VAT in its first year of implementation and the periodic tax returns received by the Federal Tax Authority from businesses registered for VAT exceeded 650,000.

Implementing VAT

VAT is one of the most common types of consumption tax that has been implemented in more than 150 countries across the globe and UAE is one of the recent additions to the list. It applies to majority of the transactions in goods and services. The registration is mandatory for all those businesses that meet the mandatory turnover threshold limit of AED 375,000/- per annum. Voluntary registration can be done if the taxable supply exceeds AED 187,500/- per year.

Registered businesses and traders will pay VAT on goods and services they buy from suppliers and these traders will in turn charge VAT to customers. The difference between the amount paid and charged will be reclaimed or paid to the government.

Businesses must report to the government the amount of VAT they have charged and paid, on a regular basis. Cases wherein they have charged more VAT than they have paid, the extra amount has to be paid to the government. If the amount paid exceeds the amount charged, that difference can be reclaimed.

VAT returns must be submitted online via Federal Tax Authority portal by the taxable person or another person who has been given the rights, within 28 days of the end of the ‘tax period’. Failure to do so will result in fine.

There are some designated zones in UAE that are treated as being outside the country for VAT purposes. For this, they need to fulfil certain criteria. Also, certain services are zero rated and exempted from VAT;

Zero Rated Goods and Services

- International transport of passengers and goods, and services related to such transport

- Supplies for certain sea, air, and land transportation modes

- New residential buildings

- Charity related buildings

- Educational services, in most cases

- Exported goods and services

- Healthcare services, in most cases

- Supply or import of investment precious metals

Areas Exempted From VAT

- Supply of certain financial services

- Residential properties – sale and lease (other than zero rated)

- Bare land – sale and lease

- Local passenger transport

When two or more people conduct business, they can apply for tax registration as a tax group. All the organizations within the group will be treated as a single entity for VAT purpose and VAT will not be charged on supplies within the entities of a group.

If a company registered for VAT fails to make taxable supplies or if the value of supplies is less than the voluntary registration threshold, then they must de-register from VAT liability. Failure to de-register within the specified time will lead to penalty.

Post Implementation Challenges

Even though it’s been more than a year since VAT came into effect in the UAE, entities still face challenges in complying with VAT regulations. A tax agent can help you out on this and ensure a smooth transition.

Tax agents are usually appointed on behalf of other people to represent them before the FTA. They act as a mediator between FTA and taxable persons and performs various legal activities prescribed by the law.

HLB HAMT is a registered tax agent in UAE; we take care of the clients’ tax obligations and represent them before the FTA.